Microfinance stress continues to affect loan originations: CRIF data

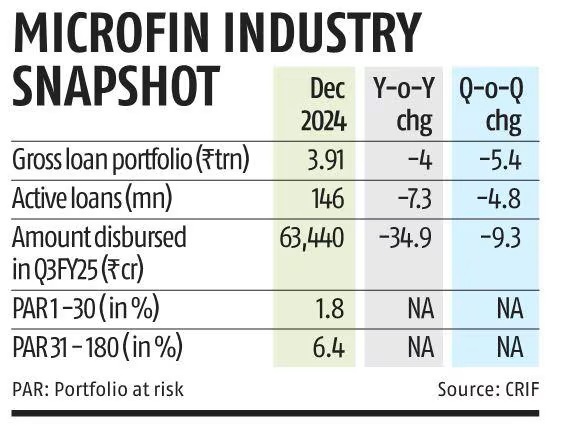

The persisting stress in the microfinance sector continued to weigh on loan originations in the December quarter (Q3FY25), with a 35 per cent year–on–year (Y-O-Y) drop in value and 42 per cent in volume, according to CRIF data.

“The contraction likely arises from rising delinquencies, borrower over-leverage across lenders, and collection inefficiencies, straining asset quality and prompting cautious growth,” the report said.

Data shows the total disbursal amount dropped from ₹97,400 crore in Q3FY24 to ₹63,440 crore in Q3FY25. In the September quarter, it was ₹69,927 crore.

The report mentioned that the industry’s emphasis on portfolio quality has led to a marked shift towards higher-ticket loans, with loans above ₹50,000 experiencing growth that outpaced the overall industry.

The overall microfinance portfolio as of December 2024 stood at ₹3.91 trillion, a 4 per cent Y-o-Y decline compared to the corresponding period the previous year, and a sequential decrease of 5.4 per cent since September 2024, driven by a series of industry calibrations, including regulatory guidelines, risk realignment and changes in underwriting and collection strategies.

Additionally, the active loans dropped from 157 million in December 2023 quarter to 146 million in December 2024 quarter, indicating a decline in supply.

“The sector remains in a recovery phase, with preventive measures and a strong focus on collections aimed at stabilising the portfolio amidst challenging industry conditions,” the report said.

It further highlighted that performance of loans in early buckets (0 to 90 days past due) has improved, as reflected in the net forward flow rates between September 2024 and December 2024.

CRIF data shows that the portfolio at risk (PAR) in the 1–30-day bucket improved by 3 basis points in the December quarter, reaching 1.8 per cent compared to 2.1 per cent in the September quarter. However, PAR in the 31–180-day bucket deteriorated by 210 basis points to 6.4 per cent in the December quarter, while PAR in the 180 days and beyond bucket worsened by 120 basis points to 3.7 per cent in the same period.

Source: BUSINESS STANDARD, 02nd April, Mumbai