MFI collections improve, but risks remain: CRIF High Mark

While some sectors show signs of stability and improvement, others, like microfinance and credit cards, require careful monitoring. Seth's analysis underscores the delicate balance between growth and risk management in the current lending environment.

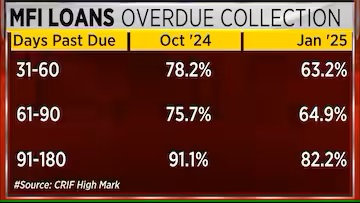

Despite persistent challenges in the microfinance sector, a glimmer of hope emerges in early 2025. Data from January indicates an improvement in collection rates, offering a potential turning point amidst rising default concerns. However, the overall health of MFI loan portfolios remains under pressure, signaling a complex landscape for lenders.

Sachin Seth, Chairman at CRIF High Mark, highlights a "silver lining" in microfinance, noting a 5% improvement in collections for loans up to 30 days overdue, and an 11% improvement for loans 31-90 days overdue.

This positive trend, however, is juxtaposed with the reality that "the default percentage has gone up," with the portfolio at risk (PAR 91-180 days) increasing from 2.9% in March 2024 to 3.6% by January 2025. The loan book size has also shrunk, indicating a cautious approach by lenders.

Beyond microfinance, Seth mentioned that credit cards with lower limits (under ₹50,000) are experiencing significant stress.

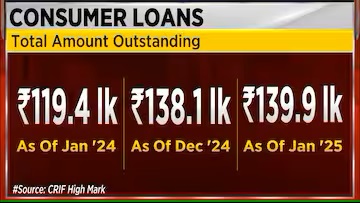

While personal loans saw rapid growth earlier, regulatory interventions have helped stabilise delinquency rates. However, this stability has come at the cost of slower growth in the personal loan book.

Initial concerns about rising defaults in two-wheeler loans have been alleviated. Current data shows that delinquency rates have returned to previous, more manageable levels.

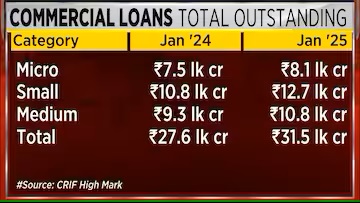

Lenders are being more cautious in extending loans to Micro, Small and Medium Enterprises (MSMEs) due to evolving definitions and market uncertainties. However, existing MSME loans, particularly those tied to commercial vehicles, are demonstrating relative stability.

Loans secured by assets like housing, property, and gold are considered low-risk and are performing well. This sector of lending is currently strong.

Source: CNBC TV18, 25th March, Mumbai